China, Rare Earths And The End Of The World As We Know It.

Our arms industry will be mothballed before the mid-terms.

Welcome to our biannual reckoning with the rare earths conundrum. In last June’s dispatch—China, Rare Earths and Intellectual Property—I asked who, precisely, will underwrite the construction of factories requiring two decades of unswerving political support, legions of scientists, millions of laborers and hundreds of billions of dollars in outlays? And what if – like Japan’s fifteen-year, multi-billion dollar effort – it yields neither a commercial profit nor even a viable product?

This month’s question is more urgent: will our defense industry implode because China’s April 25 ban on dual-use minerals exports remains in force1 after Busan? What will we do if US production of advanced weapons systems ends before America’s elections next November. There’s plenty of blame to go around.

Incredibly, the US National Defense Stockpile (NDS) holds barely three months’

supply of rare earth minerals for defense needs2 and arms-makers, like Lockheed Martin, RTX and Boeing, are no better off. And it’s not as though Congress and the White House didn’t see this coming. In 2009, after the WTO ruled in favor of America’s claim that environmental protection did not justify its REE export quotas, China lifted only partially them. Then, in 2012, President Obama complained, “American manufacturers need access to rare earth materials which China supplies but Chinese policies are preventing that from happening and go against the very rules that China agreed to follow3”. Stephen Chen explains that there’s a simple reason for China’s reluctance: “Domestic demand already outstrips supply. Export controls aren’t an aggressive geopolitical lever, they’re a rational industrial policy”.

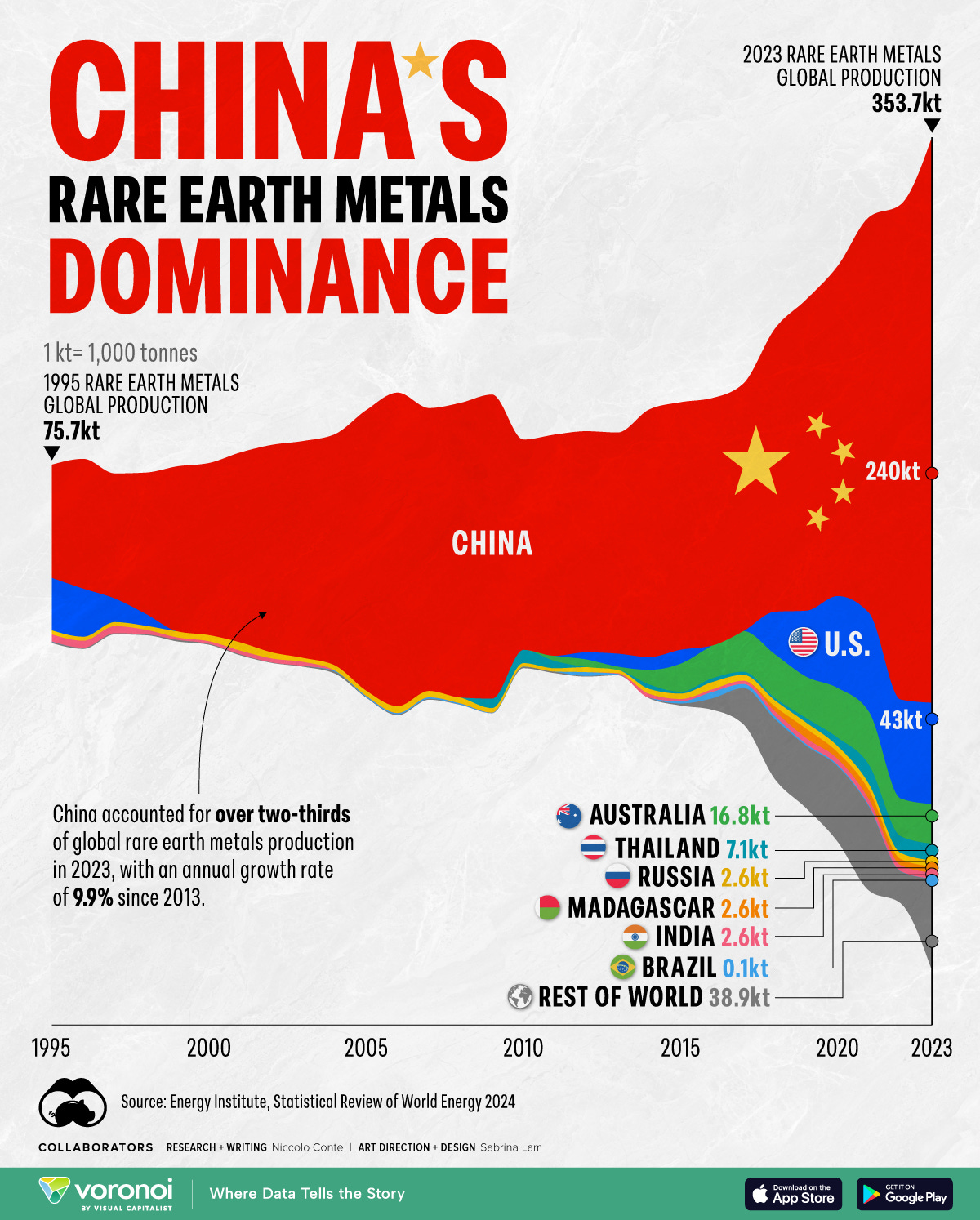

Why China dominates RE refining

In a recent interview, Treasury Secretary Scott Bessent predicted the U.S. could secure alternative supplies of REEs within 24 months, but this is fanciful. Obtaining non-rare (but banned) gallium will cause mayhem, says Arnaud Bertrand, “China extracts 146 tons of gallium annually from 20 million tons of alumina using a $150 billion factory that produces 20 million tons of alumina from a $200 billion electrolytic aluminum factory–which requires 100 billion KWh of electricity annually and which requires another $100 billion investment. These factories operate 24x7 and need 50,000 skilled workers which the US lacks, and a market to sell into, which China already occupies. Even though the technologies for gallium extraction and refining are well known, will Washington make such a vast, money-losing investment for 146 tons of gallium, an easy task compared to extracting heavy rare earth metals?”

America will capitulate

If I’m right, we’re watching the United States being reduced to a the status of a traditional Chinese client state. The New York Times headline, below, is just the first step in breaking the bad news: the world is on the cusp of pax Sinica.

To win 100 victories in 100 battles is not the acme of skill. To subdue the enemy without fighting is the acme of skill. Sun Tzu.

In Busan last week President Trump learned that China would supply non-strategic REEs for one year but supplies of dual-use minerals–scandium, samarium, gadolinium, lutetium, yttrium, dysprosium and terbium, along with gallium, germanium, antimony, graphite, REE processing technology, machinery and equipment –remain banned.

The Pentagon’s $1–2 billion acquisition push (2025–2027) aims to build reserves, but current levels cover ~6% of shortfalls in a “base case” emergency scenario. Estimates below are for defense-specific use; total industrial consumption is higher. USGS 2025, DLA solicitations, and Columbia Energy Policy Center (2025).

Critics labeled Obama’s statement hypocritical for ignoring U.S. export controls on uranium or encryption tech for security and domestic mining bans (e.g., under NEPA environmental regs), implying selective free-trade advocacy and observed that price hikes stemmed more from a weak dollar than REE scarcity.

Once again, Robert’s brings together facts, figures and insights that enable us to make sense of developments unfolding before us. This is one helluva service he provides.